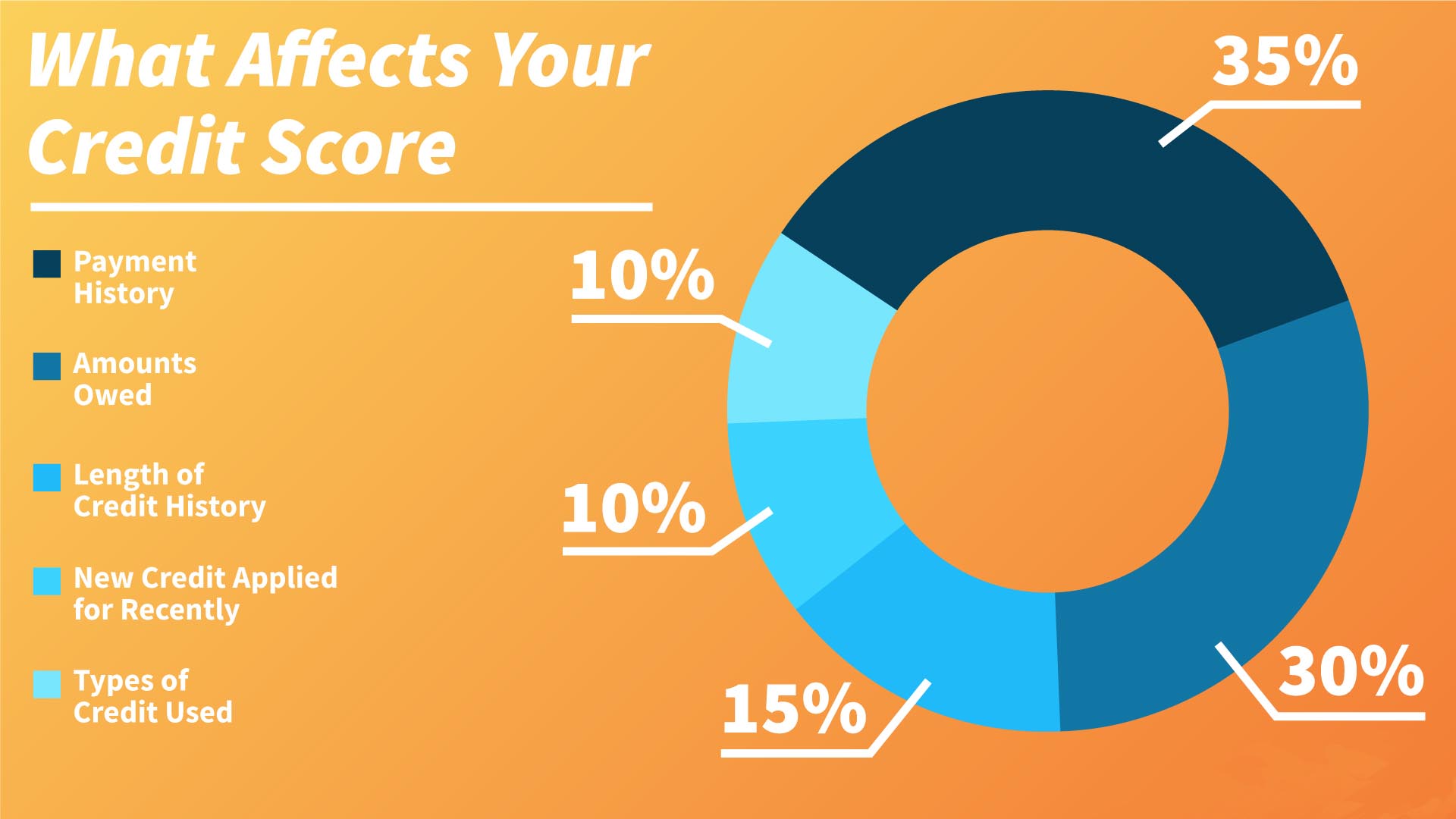

The Starting Credit Score

A credit score is a number that is assigned to people and businesses that have a financial history of borrowing and repaying debt. According to financial experts, managing this number, sometimes assigned to you when you start your first tradeline, can be overwhelming.

It is expected to be in the dark if you are unsure of what you need to do. Many people are in the dark about many areas of their finances. What is a gold IRA? When is the right age to save for retirement? What is a functional budget? These are all things we need to learn.

Surprisingly, this starting point of analyzing your financial data is a concept that is only understood by very few people. However, those who are aware can dispute any mistakes at the beginning to strengthen the foundation of this financial journey.

If you live in Los Angeles, there are plenty of resources to help you get started. One option is to seek the guidance of a credit repair attorney in Los Angeles if you have any concerns or need assistance. These professionals specialize in helping individuals and businesses improve their credit scores, dispute inaccurate information, and create a plan to manage debt. You may also consider attending financial seminars and workshops offered by banks, credit unions, or non-profit organizations in your area.

How Long Does It Take to Start Calculating Your Score?

Six months is the time most credit bureaus need to collect your financial data. So, for instance, a business that starts to repay a loan and bills today will have to wait for six months to receive its initial credit score.

Likewise, individuals’ credit scores also take the same amount of time. The credit bureaus collect data from the following sources.

- Loans and debt repayment – whether it is a business or an individual, how debts are repaid plays a major role in providing the initial data for your credit score.

- When a business starts, tradelines can establish trade lines with suppliers and other financial accounts. Companies that focus on selling credit tradelines to customers also help the newbies establish a high initial score. Then, they provide instant information to the reporting agencies, who will open a file for you.

- Credit cards – getting your first credit card without any credit score is possible. It depends on your income source and how compelling your situation is to the lenders. Once you obtain one for the first time, the reporting agencies will collect your repayment history.

What Is a Likely Starting Credit Score?

Different countries have varying models. However, the starting credit score is usually a three-figure number within the lowest and highest possible score. Therefore, there is no certain number that is assigned to every person with new credit.

The credit score could be low or high, depending on the data collected within the six-month window. So, what should a person do to get a high number?

- Have many accounts – you may be new to having a credit score, and this is fine as a credit novice. However, more accounts mean more information sent to the credit bureaus. Although having many accounts rather than only one is better, failure to manage them well will also lead to a low starting credit score.

- Repay your debts and bills – credit accounts are the main contributors to credit history. They give positive results when they are appropriately managed. Pay all the debts and bills on time to increase the chances of receiving a high score.

Conclusion

As you can see, there is no defined starting credit score. You are the one to determine what you will get by managing your credit account. Understand when they start collecting the initial data, and the minimum time they will need so that you can do the right thing.